I’ve been at this investing game a long time. Long enough to see cycles repeat themselves, cycles that I literally thought I would never again see. Yet in finance, everything repeats. You just need to keep your discipline and recognize things for what they are.

Let’s take a step back and start with a bit of a disclaimer. I’m an old-school investor. If you called me a boomer in my mentality, I wouldn’t really disagree. I still believe that things like cash flow and return on capital matter. In fact, they’re my north star. As a result, I often miss new trends, as I refuse to pay up for profitless prosperity. Sometimes, a hyper-growth company amazes me when it actually grows into its valuation, though that’s rarer than you’d think. Usually, cash flow is king, ROIC is the queen and everything else is simply stock promotion. Hence, my strong sense of skepticism towards anything new.

With that in mind, I’ve watched as AI went from an interesting parlor trick for making memes, to something that’s increasingly integrated into my daily workflow. I use it a lot and get huge value from it. I am not here to belittle AI, it’s the future, and I recognize that we’re just scratching the surface in terms of what it can do. I recognize all of this. I also recognize massive capital misallocation when I see it. I recognize an insanity bubble, and I recognize hubris.

I’m going to use a bunch of numbers here that I believe to be directionally correct, I’ve spoken with industry players who have somewhat confirmed these numbers. I fully expect that other industry insiders will quibble with these numbers, but if I feared criticism, then this blog would be no fun.

Let’s start with total datacenter spend for 2025. Insiders think it’s going to clock in at around $400 billion. If it misses that figure, it’s only because of bottlenecks that slow buildouts. Of course, it could also exceed that number, as those who are spending on these datacenters are beyond desperate to get them operational. For the sake of this piece, let’s use the $400 billion number, though it is likely a bit higher than where things may end up due to delays in construction.

What’s a datacenter made of?? There are three main components; the building and land at roughly a quarter of the cost, all the power systems, wiring, cooling, racking, etc. at about 40% of the cost, and then the GPUs themselves at about 35% of the cost. I am sure I’m off by a few percent in these categories, but I’m relying on AI and we all know it’s still imperfect. I’m assuming that the building depreciates over 30 years, the chips are obsolete in 3 to 5 years, and then the other stuff lasts about 10 years on average. Call it a 10-year depreciation curve on average for an AI datacenter. Which leads you to the first shocking revelation; the AI datacenters to be built in 2025 will suffer $40 billion of annual depreciation, while generating somewhere between $15 and $20 billion of revenue. The depreciation is literally twice what the revenue is.

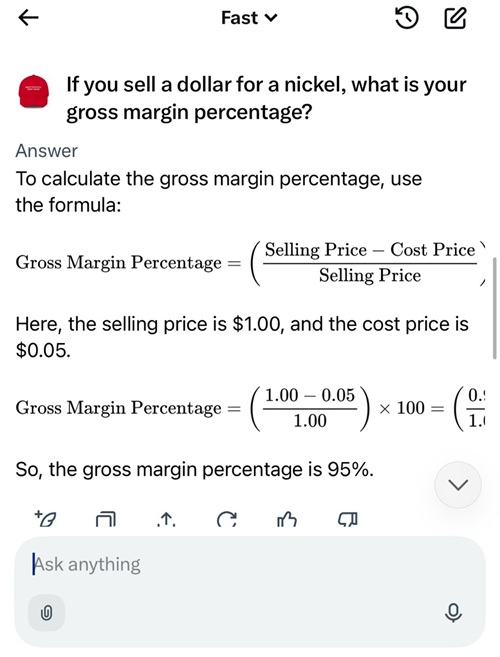

Now, here is where it gets complicated as there is no gross margin in the AI game. They’re literally giving away the technology and occasionally getting a nickel back for every dollar they give away. Calculated as a gross margin, it would be -1900%. This is the nature of trying to drive adoption and get customers attached to a product. VC has a long history of funding this sort of thing, as long as the ROIC eventually flips positive. With nothing to go on, I’m going to take an optimistic guess here, and say that ultimately, the margins get to positive, and then gradually creep up towards 25%. Why 25%?? I have no idea. It just sounds right because electricity is really expensive and you need a lot of expensive tech nerds to manage the equipment. Honestly, no one really knows where gross margins eventually land, so let’s just run with it, so that we can do some simple math. The question is, how much revenue do you need to cover the depreciation cost of the datacenter??

Hundreds of billions later, and AI is still useless when you ask it to review your math…

By my math, you need $160 billion of revenue at that 25% gross margin, which gives you $40 billion of gross margin against $40 billion of depreciation. Now, remember, revenue today is running at $15 to $20 billion. You need revenue to grow roughly ten-fold, just to cover the depreciation. Except, no one does anything to break even in business. For a new technology like this, with huge obsolescence risk, what unlevered ROIC would you demand?? Would you want a 20% ROIC?? That’s still dilutive to the ROIC for most of the largest capex spenders. Even at that dilutive ROIC, you’d need $480 billion of AI revenue to hit your target return.

Now, I think AI grows. I think the use-cases grow. I think the revenue grows. I think they eventually charge more for products that I didn’t even know could exist. However, $480 billion is a LOT of revenue for guys like me who don’t even pay a monthly fee today for the product. To put this into perspective, Netflix had $39 billion in revenue in 2024 on roughly 300 million subscribers, or less than 10% of the required revenue, yet having rather fully tapped out the TAM of users who will pay a subscription for a product like this. Microsoft Office 365 got to $ 95 billion in commercial and consumer spending in 2024, and then even Microsoft ran out of people to sell the product to. $480 billion is just an astronomical number.

Of course, corporations will adopt AI as they see productivity improvements. Governments have unlimited capital—they love overpaying for stuff. Maybe you can ultimately jam $480 billion of this stuff down their throats. The problem is that $480 billion in revenue isn’t for all of the world’s future AI needs, it’s the revenue simply needed to cover the 2025 capex spend. What if they spend twice as much in 2026?? What if you need almost $1 trillion in revenue to cover the 2026 vintage of spend?? At some point, you outrun even the government’s capacity to waste money (shocking!!)

Simply put, at the current trajectory, we’re going to hit a wall, and soon. There just isn’t enough revenue and there never can be enough revenue. The world just doesn’t have the ability to pay for this much AI. It isn’t about making the product better or charging more for the product. There just isn’t enough revenue to cover the current capex spend.

Let’s go back in time, almost three decades back. It was the late 1990s and I sent my first email. It was amazing. I then used AOL Messenger to speak with someone on a different continent. Think about the late 1990s and how innovative this was. Back then, the local telephone company would charge you extra if you made a call outside of your zip code, which was basically 10 miles away. To call a different continent would cost almost a Dollar a minute, yet here I was, speaking with someone on the other side of the earth. Think about how groundbreaking this was. It was the AI of its day. No wonder we had a huge bubble in this stuff, it was obvious that the internet would change the world.

While we all remember Pets.Com and the hundreds of other Dot Com startups that flamed away, it was companies like Global Crossing, spending tens of billions on fiber, that facilitated all of this. That fiber, amazingly, is still in use. Global Crossing went bankrupt along the way, as did many of its peers. They overestimated what people would pay for this fiber, not that it would eventually be used or valuable.

Today, I watch in awe (stupefaction really), as companies continue to throw endless resources at AI, I remember back to the Dot Com bubble and Global Crossing—fiber was the datacenter of that cycle, and Corning was the NVIDIA of its day (it lost 97% of its share price in the two years after it peaked).

I never thought we’d see another capex cycle like that one, a cycle that is almost completely devoid of revenue and profits. I really thought that the CEOs of today, educated with the lessons of the prior cycle, would never repeat the mistake of overbuilding at massive scale without revenue. Yet, here we are again. It’s bewildering.

There’s something else that this AI cycle reminds me of. Remember shale, where all the cash flow had to keep going into the ground, or oil production declined and the EBITDA covenants got tripped?? Now you have megacap tech stocks that are spending almost all of their cash flow on datacenters for fear of missing out. These asset-light businesses suddenly have the capital intensity of a shale company. Even worse, since losing the AI race is potentially existential; all future cashflow, for years into the future, may also have to be funneled into datacenters with fabulously negative returns on capital. However, lighting hundreds of billions on fire may seem preferable than losing out to a competitor, despite not even knowing what the prize ultimately is.

Carrying the thought process a step further; if there is no cash flow, and the returns on incremental invested capital are now deeply negative, why won’t these megacap tech stocks eventually be valued like a shale company at 3 times OCF?? I know, it’s crazy to even contemplate given current valuations, but if you’re on a race to nowhere, and there’s no offramp, shareholders will eventually pull the plug. We saw something similar in shale. Even the MAG7 will not be immune. Eventually shareholders will hate the capital destruction—even if at first, they cheered it on out of ignorance.

As I see it, either the arms race continues, and the megacap tech names are forced to lever up to keep buying chips, after having outrun their own cash flows; or they give up on the arms race, writing off the past few years of capex. Then again, maybe they do the write-offs, but only after their share prices are impaired as investors pull the plug. Like many things in finance, it’s all pretty obvious where this will end up, it’s the timing that’s the hard part.

Then again, I’m just a boomer with some back-of-the-envelope math here. I don’t pretend to understand technology. However, I’m a guy who understands cash flow, and there is none. I don’t see how there can ever be any return on investment given the current math. Instead, I just see endless losses, and we’re far enough along in this S-Curve, to think that we can at least start to model the returns—except they’re horribly negative. If the management teams at these megacap tech companies do not pull the plug on this adventure, eventually the shareholders will. I shudder to think about how nasty that could get for equity markets.

Remember when I pointed out how cannabis companies were terrible investments?? Usage is up dramatically since that posting, but the share prices have collapsed as no one has made any money off of it. This AI bubble is similar, but with more zeroes attached—so many zeroes, that between their capex spending, and the wealth effect that they’ve engendered, they have now effectively become a very disproportionate percentage of the growth of our economy.

At the end of the day, this AI cycle feels less like a revolution and more like a rerun. I’ve seen this story before—fiber in 2000, shale in 2014, cannabis in 2019. Each time, the technology or product was real, even transformative. But the capital cycle was brutal, the math unforgiving, and the equity holders were ultimately incinerated. AI will be no different. The datacenters will be built, the chips will hum, and some of the capacity will eventually prove mind-blowingly useful. But the investors footing the bill today will regret ever making the investment. That’s how bubbles end—not with a bang of innovation, but with the slow, grinding realization of negative returns, for years into the future. When shareholders finally wake up to the fact that AI isn’t generating cash flow, only burning it, the guillotine will fall—on management, on the stocks, and on the broader market that bet its future on a fantasy.

Caveat Emptor…

Harris Kupperman is the Founder & Chief Investment Officer of Praetorian Capital Management, and author of Praetorian Capital’s public blog, Kuppy’s Korner, from which this article has been reproduced with permission.

Information or statements provided here are opinions of the author and may not represent the opinions of Praetorian PR LLC or its affiliates. Furthermore, the information is for educational and entertainment purposes only and does not represent investment advice.