Superannuation is a tax-effective vehicle for long-term retirement savings. Currently, both contributions and investment earnings (in accumulation phase) are taxed at 15% for people with taxable incomes less than $300,000. This rate is significantly less than the highest personal marginal tax rate of 47% (2015-16 marginal tax rate plus Medicare levy of 2%, excluding the Medicare levy surcharge). Less tax paid through the accumulation phase helps maximise retirement income in pension phase.

However, there is no certainty that superannuation’s current tax benefits will remain in the medium to long term. An increase in tax payable on either superannuation contributions or earnings would reduce its appeal as a retirement saving vehicle. For example, it is rumoured that the $300,000 threshold will be reduced to $180,000 in the coming Federal Budget (the level where the additional 'Division 293' tax rate of 15% kicks in).

Superannuation restrictions

While tax effectiveness of superannuation is a key benefit, it comes with restrictions on contributions and access. A quick reminder of the main rules:

Contribution restrictions

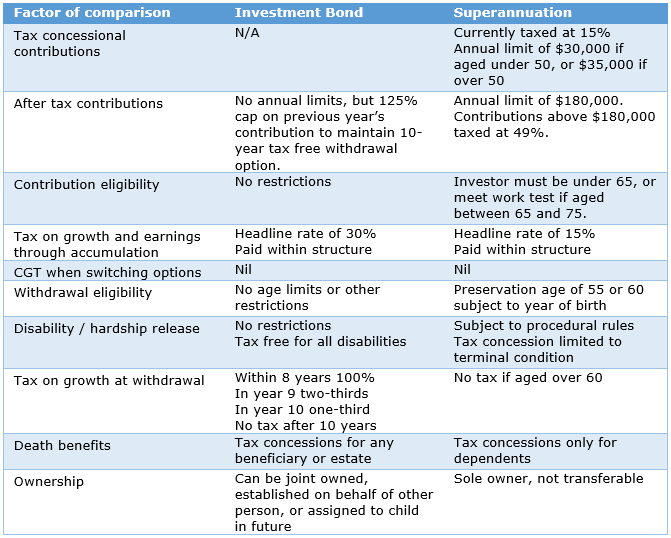

To contribute to super, the investor must be under age 65, or if aged 65 to 75, needs to meet a work test. Contributions from an employer (including amounts paid under a salary sacrifice agreement) and contributions for which a personal tax deduction is claimed cannot exceed $30,000 in a financial year if aged under 50 and $35,000 if aged 50 and over. Personal after-tax contributions (that is, non-concessional where no tax deduction is claimed) are not taxed further on amounts up to $180,000 each financial year. Where an investor is under 65, they may be able to combine the limits for up to three years to contribute up to $540,000 in a single year.

Access restrictions

Access to money in superannuation is restricted until a ‘condition of release’ is met. This generally means that the investor will not be able to withdraw or use the money until they have reached a ‘preservation age’ and have retired. Preservation age is 55 for an investor born before 1 July 1960 but increases up to age 60 for those born after this date. Earlier access may be allowed in exceptional circumstances, such as permanent disability.

Tax-effectiveness of investment bonds

An investment bond (sometimes called an insurance bond) structure can be a tax-effective vehicle which complements superannuation in saving for retirement, particularly for investors with higher marginal tax rates. A key benefit is where funds remain invested for 10 years or more, personal tax obligations are permanently removed. An investment bond also acts as a life insurance policy, and can be used in estate planning to simplify wealth transfers external to a will.

With both superannuation and investment bonds, tax is paid within the investment vehicle, not personally by the investor. Investment bonds pay a maximum a tax rate of 30% on investment earnings and growth, although franking credits and tax deductions can reduce this effective tax rate further.

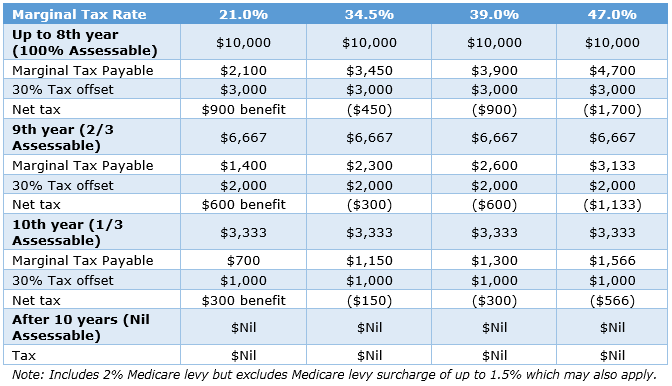

If an individual’s taxable income is at least $37,001 p.a. the tax paid on any additional personal income will be greater than on investment bond earnings. At this threshold, the marginal tax rate increases from 21% to 34.5%, higher than the 30% on investment bonds.

If the investment is fully or partially withdrawn after 10 years, the investor pays no personal income tax. If a withdrawal is made within the first 10 years, the investor will pay tax on the assessable portion of growth (100% within first eight years, two-thirds in year 9 and one-third in year 10). If investments are withdrawn within the 10 years, the investor receives a full 30% tax offset from tax already paid within the investment bond. For example, a $10,000 growth component would have tax implications for the various individual marginal tax rates as shown in the table below.

Simplicity and flexibility

Earnings on investment bonds are automatically reinvested in the bond and taxed within. Income and capital gains are not distributed to investors and do not need to be annually tracked or included in personal tax returns.

If investors’ financial goals or views change, they can switch easily between investment options within their bond without incurring any tax or Capital Gains Tax implications and without affecting the bond’s 10-year tax period.

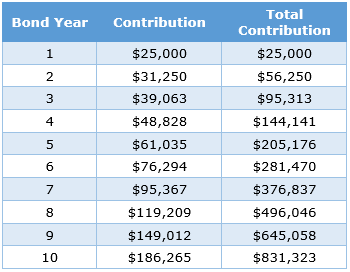

There is no limit on either the initial contribution amount or total contributions in the first bond year. Contributions can also be made at any time thereafter according to the 125% rule. As long as contributions in any subsequent bond year do not exceed 125% of the contributions in the previous year, all contributions and growth will be free of personal income tax after 10 years. This means that additional contributions can have a term of less than 10 years, and their growth or earnings will still be tax-free.

For many investors the ability to progressively increase contribution amounts over time is consistent with life events and greater disposable income, for example through paying off the mortgage, lower outgoings in school fees, or investing proceeds from an inheritance. Under the 125% rule an investor making an initial contribution of $25,000 can invest up to a further $6,250 in year 2 (in total, $31,250), and progressively build savings as illustrated in the table below.

Over 10 years, $831,323 has been contributed but only $25,000 for the full 10 years. The investor can withdraw their investment plus any growth or earnings tax-free at the end of the 10-year term. Or the investor may keep the investment bond open and make additional contributions beyond 10 years with these investment amounts also tax-free on withdrawal.

Caution is needed in relation to additional investments that exceed the 125% limit in any year, as the 10-year tax period will restart from the year in which the excess contribution is made. In a similar vein, if the investor does not contribute in a particular year, then a contribution in any subsequent year will restart the 10-year tax period. Either of these might be a deliberate investment strategy, or be the result of a life event impacting the investor’s ability to contribute. However, with a minimum additional investment of $500 per year there is great flexibility for investors to maintain their 10-year tax benefit.

Flexible estate planning

An investment bond’s life insurance component enables tax-effective estate planning and simple wealth transfers external to a will. It gives the life insured significant flexibility and control in determining beneficiaries of any ‘death maturity’ payments.

In superannuation, death benefit tax concessions apply only to dependents of the life insured. However, an investment bond’s death benefits can be directed tax-free to any nominated beneficiary, including adult family members, or the estate. How long the bond has been held does not impact the tax-free status. This flexibility may reduce the risk of disputes over estates and enable benefits to be paid more quickly.

Investment bonds can also be established on behalf of children, providing simplicity in managing the tax that applies to children’s income. It may also be assigned to a child in the future (subject to parental or guardian consent) without tax or legal complications. The child has the option to continue holding the investment bond without affecting the original 10-year tax period start date.

Summary comparing superannuation and investment bond strategies

Neil Rogan is General Manager of Centuria Life’s Investment Bond Division. Suitability of investment bonds will depend on a person’s circumstances, financial objectives and needs, none of which have been taken into consideration in this document. Prospective investors should obtain professional advice before making a decision to invest.