Every investment demands a compromise. The long-term upside of shares comes with short-term downside risk and a potential permanent loss of capital. Government bonds are capital secure but with lower income and they will never be worth more than par at maturity. Any number of risks can hit a property investment, even in the best of locations. In assessing these trade-offs, Buy-Write (sometimes also called covered call) funds offer a mix that may appeal to some investors in the current circumstances.

Buy-Write strategies forgo some of the potential upside in the stockmarket in exchange for enhanced income (above equity dividends). It entails buying or owning a stock or portfolio and simultaneously selling a call option against it. The investor earns extra income by retaining the premium received from writing the call. However, in giving someone else the right to buy a share at the call price, some upside potential is removed.

(The strategy is usually called a covered call if the shares are already held and the option is written against an existing portfolio. For this article, we will use the terms interchangeably).

The S&P/ASX Buy-Write Index

The ASX provides an index based on holding the S&P/ASX200 portfolio of stocks and selling (or writing) an index call option for income. The S&P/ASX Buy -Write Index (ASX: XBW) is plotted below against the usual S&P/ASX 200 accumulation index (ASX:XJO). The ASX describes the Buy-Write index in more detail here.

"In the case of the XBW, the underlying security is the S&P/ASX 200 Accumulation Index over which a S&P/ASX 200 Index call option is sold each quarter. Once an option series has been selected and a short option position established, the option position is held to expiry."

The comparison of XBW (with the option) and XJO (the normal index) using a Market Index chart shows the red line, the ASX200, outperforms the Buy-Write version, the blue line, during rising markets, and then the options strategy does well in flat or falling markets. Over the last five years, XBW has outperformed XJO.

How Buy-Write works and potential yield enhancement

The advantage of using a fund for a Buy-Write strategy is that the options and investment buying is done by the fund manager, but let's illustrate how it works using one stock. Let’s say you own 1,000 Company A shares at $20 worth $20,000 and you would like more income from them, and you are not expecting the price to rise in the short term. A Buy-Write (covered call) strategy could be to sell 1,000 June 2023 $22.00 call options at $1.00, generating income of $1,000 or 5% of the value of the shares.

At expiry, the so-called 'break-even' for the strategy is a share price of $19.00 ($20 minus $1), or a fall of 5%. If the market does not change, the shares are still worth $20,000 but the gain is $1,000 for the expired option. The option holder does not exercise the right to buy at $22 because Company A is cheaper on the market.

If Company A shares rise to $25, there is an increase in value of $5,000 on the shares but a loss of $3,000 on the option, but with the $1,000 of option premium, the gain is $3,000 ($5,000-$3,000+$1,000) from holding Company A and selling the call instead of $5,000 from simply holding. This shows how Buy-Write strategies give away some of the upside in a strong market.

According to the ASX, Buy-Write options are the most common options strategy on the exchange, although the focus in this article is on the funds that adopt the technique, not individuals.

Why the timing might be right

There are many reasons why equity market returns over the next few years might not be as good as the excellent period from 2012 to 2021. This favourable time was characterised by falling and low interest rates and inflation, the rise of dominant technology stocks such as Apple, Google, Microsoft and Amazon, and the S&P500 rising a healthy 17% per annum for 10 years to 2021. The end of this period also saw generous monetary stimulus during the pandemic from central banks around the world which powered a recovery, but there is now a payback period underway.

At no time in the last decade did the world experience a war as threatening as the Ukraine conflict, in which either Russia will eventually win and continue its push westwards, or Ukraine will win, and Russia’s final fling may include a nuclear threat. Global supply chains have faced realignment and future demographic changes in China, Japan and much of the west will challenge economic growth. The world faces massive costs in decarbonising with dislocations in energy supplies. Interest rates have risen quickly and bank lending standards are tightening.

Investment conditions are simply not as favourable as in the previous decade. At the latest Annual Shareholder Meeting of Berkshire Hathaway, Warren Buffett warned that the recent success of his companies after a strong growth period is now winding down, and “The majority of our businesses will report lower earnings this year than last year.”

There are two main reasons why covered call strategies should outperform during bear markets.

First, income from selling calls partly offsets falling share prices, especially as call options are less likely to be exercised. More of the option premium is retained.

Second, volatility is usually higher during major bear markets, and premiums are larger from selling calls. The fund manager hopes the options market is overpaying for the opportunity to benefit from rising share prices.

Australian funds that use Buy-Write

Many Australian funds write call options against their portfolios to generate income, but investors should ensure the funds acknowledge two things:

- It is not a silver bullet to magically generate free income, as it gives some (perhaps most) of the upside to the options buyer.

- The fund is likely to underperform in a strong bull market. Investors should not be critical of the fund manager if this happens, assuming it is due to the structure and not poor stock selection.

Here is a sample of Australian Buy-Write funds:

1. First Sentier Equity Income Fund

First Sentier has run this strategy with the same team since 2008 and identifies three sources of income: two are the traditional streams generated from dividends and franking credits, and the third is the option premium income. In contrast to other equity income strategies, the managers do not specifically target high dividend companies, but look for the best investments including growth stocks which do not pay high dividends.

First Sentier quote the example of realestate.com (ASX:REA) which is not normally in an equity income fund because its dividend yield is only around 2%. But hidden in that number is a rapidly-growing income stream, driving a rising share price, so the income grows although the yield stays at only 2%. The income received from REA has been 40% dividends, 15% franking credits and 45% options premium. However, a bigger dividend payer such as CBA delivers income from 70% dividends, 20% franking credits and 10% options premium.

The fund outperforms in the vast majority of down months because it is collecting options premiums, but should be expected to underperform in a strongly-rising month.

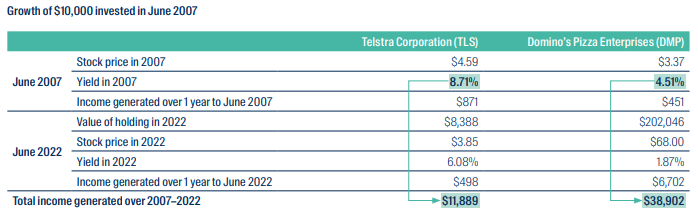

This specific example provided by First Sentier comparing Telstra with Domino’s Pizza shows although Telstra offered the bigger dividend yield in 2007, a much larger income stream has been achieved from the faster-growing pizza company.

2. JP Morgan Equity Premium Income

The JP Morgan Equity Premium Income ETF (ASX:JEPI) is an Australian-listed version of the largest actively-managed ETF in the US, with assets over US$24 billion. It delivers regular income and exposure to the S&P500 with lower volatility. It sells one-month, out-of-the-money call options to generate income but JP Morgan is clear that it may forgo some of the market’s upside.

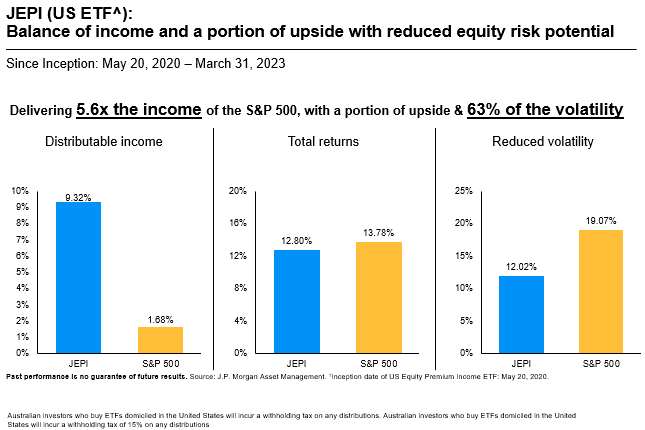

This chart from JP Morgan Asset Management shows how much of the distributable income on the US fund relies on the options' value. Typical of covered call funds in a rising market, its total returns are less than the S&P500 as it misses some of the upside, but with significantly less volatility.

3. Global X Covered Call ETFs

ETF issuer Global X has introduced a range of covered call funds to the local market including the Global X S&P/ASX 200 Covered Call ETF (ASX:AYLD). The fund holds the companies in the S&P/ASX 200 index and sells at-the-money call options on the same index on a quarterly basis to generate income. It aims to track the performance of the S&P/ASX Buy-Write Index as described above. Australian investors also have access on local exchanges to the Global X Nasdaq 100 Covered Call ETF (ASX:QYLD) and Global X S&P 500 Covered Call ETF (ASX:UYLD) which are among the largest covered call strategies in the world.

Generally, Australian Buy-Write funds do not rely on selling options for as much of their income because Australian companies pay higher dividends than US companies.

Other funds may use a range of strategies designed to generate multiple sources of return, such as the Talaria Global Equity Fund (Managed Fund) (ASX:TLRA) which is part of the Cboe stable of funds. It uses various options techniques including Buy-Write, and the call option is always fully equity backed so there is no added leverage from the options position.

Also in ETFs, the three Betashares funds, Equity Yield Maximiser (ASX:YMAX), S&P500 Yield Maximiser (ASX:UMAX) and NASDAQ100 Yield Maximiser (ASX:QMAX) also use Buy-Write and combined hold over $500 million in assets.

Djerriwarrh (ASX:DJW) is a $750 million Listed Investment Company that maintains options coverage in a range of 30% to 40% to generate income, and is currently at about 31%.

Buy-Write suitability for particular investors and markets

A Buy-Write fund is not a typical equity fund which gives exposure to the stockmarket and its returns rise and fall directly with the market and the ability of a fund manager to select stocks. Rather, it comes with a particular investment proposition that may not capture all the market upside in return for collecting options premiums. The strategy will tend to outperformance in flat or falling markets but not in strongly-rising markets.

Graham Hand is Editor-At-Large for Firstlinks. This article is general information and does not consider the circumstances of any investor. The strategy offered by the funds mentioned in this article involve using options which may be more difficult for some investors to understand, and financial advice may be warranted.