Australia’s capital gains tax has been in the economic and political spotlight for much of the year, with a number of substantial proposals put forward for reform. Ironically, it turns out that the simplest and fairest path forward is the one where we wind the clock back to pre-1999 and directly remove inflationary gains through indexation.

The main proposals to reform the tax treatment of capital gains include a reduction in the discount, taxing assets at different rates, and removing the discount to replace it with cost-base indexation.

As previous e61 research argues, an indexation-based system would improve the current treatment of capital gains. By taking into account the unique circumstances of the investor, indexation is a fairer and less distortionary way of taxing capital gains.

This would be a significant reform, and even more so if it becomes the first step toward taxing capital income consistently with other income over time.

A coherent goal for an income tax is to tax increases in economic capacity – or real income – as a measure of someone’s ability to pay. Once this is recognised, the problem with the current capital gains system becomes clearer. The existing CGT discount, and many of the reform options proposed, do not consistently tax real capital income. Indexation does.

Consistency is not as simple as taxing every dollar received in the same way. The tax system recognises that income is the money that remains after subtracting the costs incurred to generate it. Businesses deduct operating costs. Individuals deduct work-related expenses. These adjustments are not concessions but are necessary to measure true income.

Inflation is a cost for holding savings. The capital gains discount recognises this and attempts to approximate this cost in a way that is simple to comply with and administer.

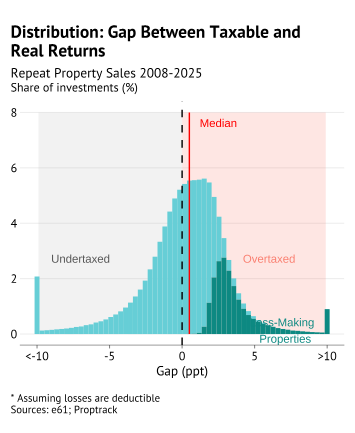

However, it just isn’t a good approximation. The correct discount depends on the rate of return on the asset – where assets with high rates of return are less exposed to inflation and require a lower discount.

As recent e61 research has shown, there is a large spread in capital gains returns. For example, among housing investors between 2008 and 2025 those with low returns (the bottom quartile) made at least a 1.6% real loss while those with high returns (the top quartile) made over a 5% real gain. Such a spread implies individuals would need very different discounts to account for inflation costs, something that the current 50% discount and many of the proposed reform options fail to account for.

For this reason, cost-base indexation – increasing the cost base by a measure of inflation – would more accurately capture the real capital gain than a flat-rate discount. Such an approach allows for variation in inflation exposure across assets and holding periods – thereby ensuring that individuals are taxed on their full real capital gain, no more, no less.

How to tax capital income like wages

An equivalent way of understanding indexation is that it is an attempt to tax a form of capital income like wages. As shown in our e61 tax calculator release, indexation is necessary to ensure the real income from labour and capital are taxed the same way.

However, as our Submission to the Senate Select Committee on the operation of the capital gains discount highlighted – in the absence of inflation – there were two other reasons why the treatment of capital gains needs to be adjusted.

- Ensuring symmetry: if only real returns are taxed due to indexation, then only real financing costs should be deductible. The failure to do so encourages excessive borrowing as outlined in our note on housing leverage.

- Smoothing taxation over time: capital gains are lumpy, which means that they end up taxed at higher rates than if they were smoothed over time. This either encourages strategic avoidance/timing or is simply inequitable. Allowing some form of income-averaging/accrual treatment would mitigate this.

The logic of inflation adjustment, symmetric treatment, and smoothing doesn’t just apply to capital gains, it also applies to all types of capital income. When inflation erodes the real value of an asset, part of any nominal return simply compensates for that loss. Taxing this component is equivalent to taxing a cost. It results in an effective tax rate on real returns that can be far higher than intended, and in some cases can lead to positive tax liabilities even when real returns are negative.

If we genuinely want to tax wages and capital income consistently, we need to start by measuring both on a comparable basis. For wages, the tax base is already close to a real measure of income, as it reflects payments for current labour rather than the revaluation of past savings. For capital income, achieving the same requires explicitly adjusting for inflation.

An inflation, leverage and timing neutral system

These three principles are reflected in our proposal for an ILT-neutral (inflation, leverage and timing neutral) system for taxing capital income, including capital gains. This proposal only taxes the real component of capital income, only allows real financing costs to be deducted, and smooths volatile sources of income for assessing tax liabilities.

There are also arguments for going further. A large literature highlights that the 'normal' rate of return to capital should not be taxed. When a saver chooses to invest rather than spend, they require a minimum 'normal' return simply to make that deferral in consumption worthwhile. Taxing this component is, in effect, a tax on the decision to save rather than any gain from it. Under this approach, only returns above this normal rate would be taxed.

This can be implemented through an allowance for a normal rate of return, applied uniformly across assets. Conceptually, this would simply extend the inflation adjustment: instead of excluding just inflation, the tax system would exclude both inflation and the risk-free real return, taxing only excess returns.

The key point is that reform of capital gains taxation is just a first step in a broader evaluation of the taxation of capital income. Once we recognise that the objective is to tax real income, it becomes clear that the broader system for taxing capital income requires a more coherent and consistent framework.

Recent engagement on tax policy – through the Senate inquiry, Allegra Spender’s tax white paper, and the McKinnon tax summit – reflects a growing community appetite for meaningful tax reform, and a willingness to move past the narrow winners-and-losers framing of past debates. A shift to indexation would meet part of that demand.

Governments are often critiqued for a lack of engagement on tax policy. However, this time has been different. Its willingness to listen and encourage public debate has led to a richer understanding and evaluation of capital gains taxation alternatives.

Greater engagement by the public, a government willing to hear varying positions, and a broader civil society willing to make good faith arguments about tax policy are all positive signs for future tax reform. In this context, any reform announced in the upcoming budget should be seen not as the end of the conversation, but as the start of a longer program of repair.

Matt Nolan is a Senior Research Manager at the e61 Institute. His research is focused on analysing income distributions using microdata, with a focus on how taxes, transfers, and changes in labour market settings influence the distribution of income. Matt previously worked at the Inland Revenue Department of New Zealand and as a teaching fellow at Victoria University of Wellington. He holds a PhD in Philosophy (Economics) from Victoria University of Wellington.