Markets are off to a good start to the year, and we still see opportunities in several exciting themes for this year and beyond:

1. Winners in alternative assets (‘alts’)

One of the less obvious ‘fly wheels’ Montaka identified several years ago was in the business models of the world’s leading alternative asset managers – particularly Blackstone and KKR. We observed that, in the asset management industry, growth disproportionately favours the largest, biggest, most trusted brand names, with the longest track records. This greater scale drives advantages in talent attraction / retention, access to deal flow, geographic and product diversification, and client attraction / retention – which further drives scale, and so the flywheel continues to gather steam.

Source: Morningstar.com

The alternative asset management space is undergoing a large structural transformation that we believe will result in super-normal asset growth over the coming decade – and will disproportionately favour the leading managers. The industry, at approximately US$10 trillion aggregate assets under management (AUM) today, has significant room to grow in the context of global stocks and bonds of more than US$200 trillion, and real estate an additional US$100 trillion. Growth will continue to be driven by (i) Insurance partnerships – which represent a US$30 trillion pool of assets; (ii) Retail / private wealth channels – which represent more than US$80 trillion in assets; and (iii) Asian allocations to alts – which are currently running at a penetration that is one-quarter that of North America.

While this structural transformation of the alts space remains in an early innings, it is coming – and we think it is underappreciated by the market.

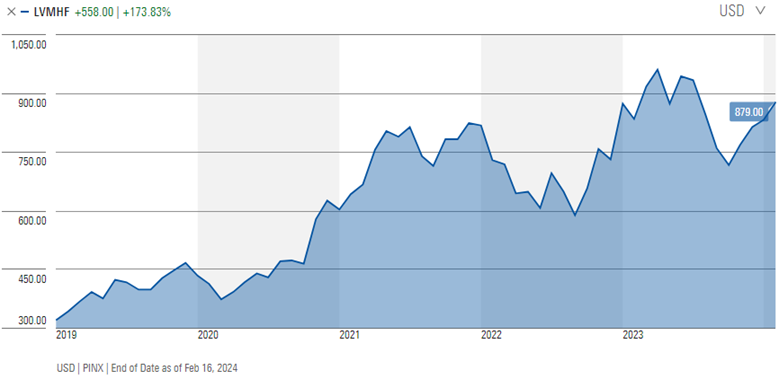

2. A consumer luxury winner

LVMH owns several of the world’s most prestigious and well-nurtured luxury brands, including Christian Dior and the 170-year-old Louis Vuitton. Its patient, methodical brand-nurturing over decades (not months or years) under founder, Bernard Arnault, enables the group to continue to grow strongly in a luxury market that is seeing demand for competing offerings soften.

Source: Morningstar.com

This long-term approach to value-building is less common than it should be, but refreshing, nonetheless. In recent days, Arnault reiterated that ‘growth at all costs’ is not the goal. And that he is very happy to deliberately slow his brands’ growth to preserve and enhance long-term desirability.

In a world in which the wealthy continue to grow wealthier, LVMH’s best customers have an extraordinary ability to pay almost any price for the world’s most luxurious goods. Price increases – even substantial ones – are not questioned, or even noticed, by these customers. And indeed, higher prices only serve to increase the cachet and exclusivity of these brands. As a result, long-term revenue growth will likely continue to be driven by price increases to an unusually large degree.

Such a strong contribution to growth from pricing has important profit margin implications for LVMH. It means that long-term profit margins will probably end up at levels far greater than those being expected by the market today. And this is one of the important reasons we believe this extraordinary business is undervalued today.

3. Winners in AI

It will come as little surprise to regular readers that our portfolio is meaningfully exposed to those select businesses we assess as high-probability long-term winners from the AI revolution – which remains in its infancy.

We see AI winners across three basic dimensions:

- Those that can ‘distribute’ the benefits of AI to customers. Winners along this dimension will likely be dominated by businesses with existing large, privileged datasets, and large embedded customer bases. These include the likes of Microsoft, ServiceNow, Salesforce, and Spotify.

- Those that can employ AI successfully in their own operations to increase productivity. Early winners along this dimension include Meta and Alphabet – though longer-term winners will span lots of non-tech industries as well.

- Those that sell the compute, and related services, required to run the AI-infused software applications. Along this dimension, the three hyperscalers – Amazon, Microsoft and Alphabet – are the clear winners in the western world. (Alibaba and Tencent continue to appear to be the highest probability winners in the second largest economy in the world, China).

After some strong stock price performances in 2023, the temptation is there for some investors to perhaps wonder if the ‘AI thesis’ has already largely played out. We strongly caution against such a view. Indeed, our research shows that, for most large enterprise clients, early experimentation is underway, however, large-scale rollouts of AI-infused applications have not yet even begun.

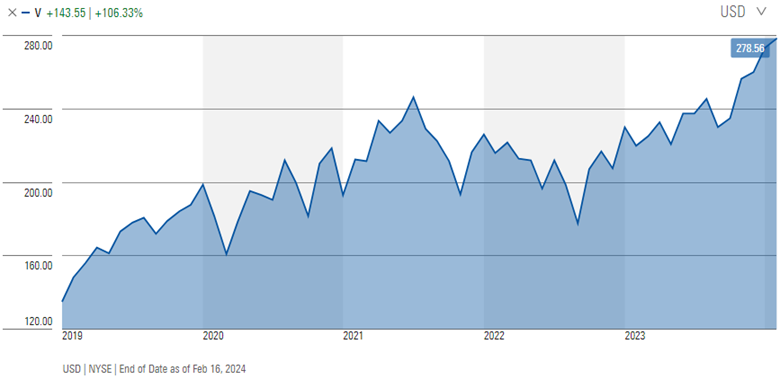

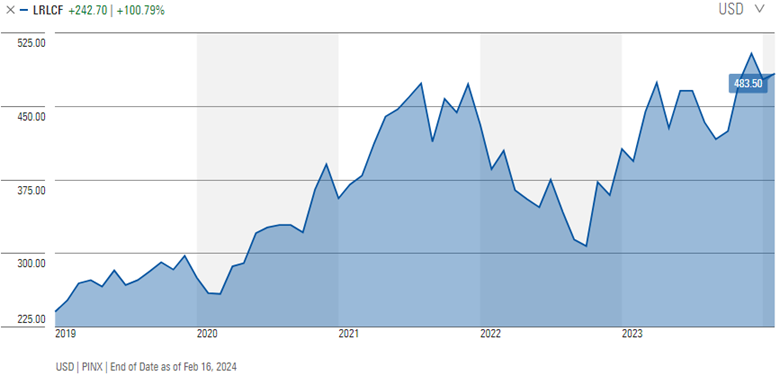

4. Mission-critical financial services platforms

There are several financial services platforms out there today that are so mission-critical, one does not need to lose sleep over whether or not the businesses will exist over the longer term. Identifying these businesses is relatively straightforward. It is far more challenging to identify a subset of these businesses that are mispriced by the market today and materially undervalued. We believe we have currently identified two.

S&P Global owns some of the world’s largest and most valuable financial datasets and has built several important businesses on top of these advantages. One of its most valuable is its Ratings business which provides credit ratings for the world’s fixed income securities. Of course, this business won big from the significant bond issuance that happened when interest rates were very low during the pandemic – and demand was pulled forward. But when rates started to rise, S&P Global experienced an ‘air pocket’ and demand temporarily evaporated.

Source: Morningstar.com

But while Ratings earnings are currently depressed, the market is not adequately reflecting the large earnings uptick that will materialize over the coming years. Substantially all of the bonds issued over the last three years need to be refinanced. The demand for S&P’s ratings is simply pent-up. It is coming. Indeed, between now and 2026, S&P Global expects that US$8 trillion in refinancings will need ratings.

Visa is the world’s largest global payments network and probably needs little introduction. What is underappreciated about Visa is the long-term compounding effect of its relatively newer, smaller, but higher-growth businesses in Visa Direct and B2B / Commercial payments – and the various services that will be attached to these over time.

Source: Morningstar.com

Today, most of the market is myopically focused on Visa’s large core consumer payments business, which is slowing now after a booming period fuelled by fiscal stimuli and high inflation. But the longer-term contribution from Visa’s newer businesses will likely be more than the market currently expects due to the compounding effect of their relatively higher growth rates and very large addressable markets.

5. Digital marketing gatekeepers

The world’s digital marketing gatekeepers – think Meta, Alphabet, Amazon and Tencent in China – continue to grow in importance for the revenue-generation of businesses, large and small, and from substantially all industries. As businesses become more sophisticated in harnessing their customer data, and the digital marketing platforms grow in sophistication with data-based targeting and measurement, buyers and sellers are increasingly connected for transactions that would otherwise have not been made. As a result, the willingness to pay for these services by advertisers continues to grow structurally.

This dynamic is best illustrated with a simple example from 2023. L’Oreal, the world’s largest cosmetics company, has consistently grown its revenues at around 15% per annum of late, in a global cosmetics market that typically grows only around 6 or 7% per annum. The reason for this extraordinary outperformance is increasingly larger allocations to sophisticated digital marketing spend.

Source: Morningstar.com

L’Oreal spends approximately €14 billion per annum on advertising and promotions (A&P) – of which, 75% is allocated to digital media. In 2024, it will grow this spend by another 16% over and above 2023 levels. “We are developing our own AI-powered A&P allocation tool,” L’Oreal’s CEO, Nicolas Hieronimus, said last year, “which gives spectacular results in terms of increasing ROI both short-term and long-term.”

Through this lens, the world’s digital marketing gatekeepers hold the key to unlocking new sales for businesses across a wide range of industries that otherwise would not be made. This makes them, in effect, quasi-shareholders in nearly every other business on planet earth. And we believe this continues to be underappreciated by the market.

Andrew Macken is the Chief Investment Officer at Montaka Global Investments, a sponsor of Firstlinks. This article is general information and is based on an understanding of current legislation.

For more articles and papers from Montaka, click here.