The advent of Artificial Intelligence (AI) is affecting ever expanding fields of human activity. And the way we invest is no exception. It’s never been timelier for investors, advisors and investment managers to take deep stock of the impacts, real and potential, of AI, so we can better prepare to manage them – whether by leveraging opportunities, managing new risks or, more likely, both.

This article summarises a recent discussion paper containing insights into AI and, in particular its effects – current and future – on both the way we invest and how investments are sourced, implemented and managed.

Not all machine learning is AI

For the purposes of this article, we define AI broadly as “a machine’s ability to perform the cognitive functions we usually associate with human minds”.

Importantly, while all AI relies on the kind of machine learning that we may already be familiar with, such as algorithms that push certain information our way or trading apps that monitor and act on market changes, not all machine learning is AI. Rather, AI is characterised by the added nuanced ‘human’ and ‘cognitive’ aspects evident in the way a machine ‘makes decisions’ based on inputs, rules and using the resulting connections that govern its ultimate outputs.

Eight ways AI will affect the way we invest

There are eight key areas where AI is likely to affect, or continue to affect, the way we invest. These areas further divide into ‘personal’ and ‘institutional’ impacts.

The role of AI in advice and personal investing

1. AI the great equaliser? Boosting financial literacy

Financial literacy has been falling in Australia and is lower among women and younger people than the general population1. Further, without higher literacy, the sheer volume of online ‘financial’ information increases susceptibility to inaccuracy and misuse – the Gamestop and cryptobubble experiences are cases in point.

AI offers a prime opportunity to boost financial literacy, especially given that a lot of existing fintech is already popular with younger people: as many as 20% use automated savings tools and more than 50% hold some kind of investment. Use of digital assistants, already widely accessible, can also help overcome the barrier of uncertainty and fear of seeming ignorant.

Against this backdrop of opportunity, perhaps the major immediate barrier to using AI to boost financial literacy is slowness and inconsistency in incorporating financial literacy as core curriculum in schools.

2. Freeing advisors to grow business and focus on the personal: AI for advice and analytics

Artificial intelligence is already changing the way advice is delivered. It can dramatically reduce administration, reporting and communication loads, update legal changes, support client on-boarding, portfolio rebalances and so on – all customisable for client and advisor.

This allows the advisor to focus on the most important part of advice – the human factor. The personal touch becomes more significant because, as it currently stands, AI is broad, not deep. Despite many attempts, it can’t provide the depth of knowledge and personalisation required for genuinely tailored advice.

Scepticism about AI is also common, perhaps deepened by the older skew of both advisors and clients. Further, as a senior advisor recently pointed out: “AI is not likely to prevent a client from panic selling at the bottom”. Or not yet anyway.

For advisors, then, AI offers significant opportunities to maximise the number and quality of client relationships and expand business development by freeing them from more routine administration and compliance.

3. Stock selection and trading using AI: still stuck on the transactional track

Despite their proliferation, very few trading apps seem to incorporate significant AI. Apps tend to compete on usability and cost rather than the intelligence of their research or advice. Significantly, some apps offer traditional financial services, highlighting the importance of the human side and more holistic services, rather than pure tech or AI.

The role of AI in institutional investing

4. More time for research and adding value: automated coding and reporting

In the institutional context, the speed and volume at which AI can summarise and report on markets and research, with the length, detail and content focus pre-specified, gives portfolio managers more time for value-adding activities such as research.

For example, the 3,600 word Reserve Bank of Australia’s Statement on Monetary Policy August 2023: Economic Outlook report was summarised into 200 words in just four seconds.

AI coding is also a timesaving gamechanger. Chat GPT can write code fast and accurately. For example, code to chart or track any available data (for example, inflation), and software that will write natural language into the coding of choice, can now be easily used.

The proviso here is that, as with all AI, the quality of outputs is dependent of the quality of inputs and weights (that is, the linkages set up to help guide the decision model). This is especially the case because current options are public and generic, potentially lacking nuance, accuracy and depth, although more sophisticated options are coming onstream.

5. Mining hidden alpha though pattern recognition and topic modelling

It’s the nature of humanity to look for patterns where they may not exist, and the role of human cognitive bias in finding patterns is well established.

AI is not only free of those cognitive biases, but it also has the potential to capture and analyse data at volumes and speeds not possible for humans. That includes the ability to see similarities or differences among topics, groups or clusters that would be beyond the usual scope of human analysis. This offers the very real potential to exploit previously hidden alpha sources.

6. Finding the wheat in the chaff: Natural Language Processing and summarising unstructured data

We know AI can support swift access and analysis of structured financial information such as reports, market prices and volumes and so on.

However, much financial information is unstructured, known as ‘alternative’ or ‘alt’ data. Examples include textual reports or news, images, point of sale or weather data, all of which can have a significant impact on investment performance and outlooks. It is here that AI – perhaps unexpectedly – can offer significant value, primarily using Natural Language Processing (NLP).

NLP can extract useful information from news, spoken word transcripts, regulatory reports and other sources, allowing measurement of the underlying intent, concerns and sentiment. Extracting such sentiment or tone from a company CEO or CFO may help assess future price or earnings.

At RQI Investors we have used NLP by inputting the AI with a domain specific dictionary, along with words and phrases that signify positive and negative sentiment. From there, it can be trained to identify more nuanced language that may indicate performance or prospects. As well as written texts and images, it can analyse ‘live’ language via transcripts, including more fluid contexts such as Q&A sessions or conference calls at earnings announcements.

Examples of such language nuances include:

- A filibuster signal for management that speak for too long

- An obfuscator signal for management that use speech which is too complex

- Sentiment or tone signals based on both prepared management speech and more free-form Q&As

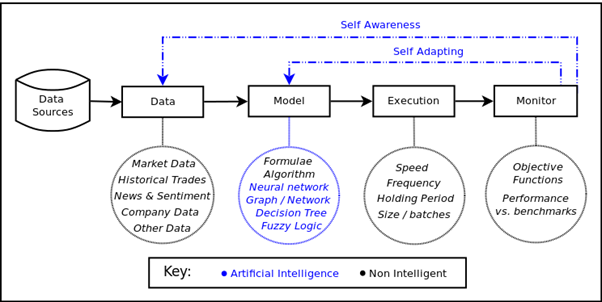

7. Trading algorithms: automated flexibility and adaptability but still a way to go

Conventional trading algorithms are based on setting up objective functions and other customised criteria – maximise profit, or minimise net exposure, and so on. While non-AI models are fairly simplistic, enhancement with AI allows for more variables and can be built to adapt and learn from news or order flow ‘on the fly’.

Conceptual Algorithmic Trading System

Source: https://www.turingfinance.com/dissecting-algorithmic-trading/

AI trading algorithms can adjust and reweight data sources automatically, and the algorithm itself can be adapted and optimised while in use, or as part of the training process.

Thus, AI can support a more nuanced and flexible trading platform that is adaptive to circumstances and market conditions. However, its work can be difficult to monitor and understand and is heavily reliant on historical data and its performance is dependent on the quality of its platform.

8. Portfolio optimisation: tackling the complex problems

Traditional manual portfolio construction works well when the market or portfolio behaves ‘as it should’. It is when the market ‘misbehaves’ that AI construction can come into its own, enabling us to divide and analyse data differently, more quickly and in particular, to address more complex problems.

A prime example is forecast errors in returns or alphas, which are problematic for conventional optimisation techniques. Here, AI that learns which return forecasts create problems can be employed, aiming to iteratively or sequentially train the model to handle outliers or errors better.

AI is here to stay

Using AI in investing is already shown to improve efficiency and financial knowledge and has vast further potential to add value through clever implementation of ideas, improved trading and portfolio construction.

The big truth? AI is not going away. While it is certainly not the universal panacea and will never replace the power of human thinking and ingenuity, for investors, advisors and investment managers, staying close to the latest AI applications and using its potential intelligently alongside their own unique human skills and experience will be the key to success.

Download the full paper here. In addition to the investment-related discussion, the paper canvasses some of the broader societal and ethical issues raised by AI, including its impact on work and some interesting detail about the creation of different AI models.

1HILDA Survey (2016-2020). Household, Income and Labour Dynamics in Australia (HILDA) Survey from the Melbourne Institute.

Dr. David Walsh is Head of Investment at RQI Investors (previously known as Realindex Investments), a wholly owned investment management subsidiary of First Sentier Investors, a sponsor of Firstlinks. This article is general information and does not consider the circumstances of any investor.

For more articles and papers from First Sentier Investors, please click here.